Wyden's crypto quid pro quo

What Senate Finance Chair Wyden did for crypto firm FTX and its now-felonious founder Sam Bankman-Fried to earn a big wad of campaign loot

As you probably know, a federal jury last week found cryptocurrency firm FTX founder Sam Bankman-Fried guilty on seven counts of fraud and conspiracy to launder money. What follows is my attempt to set forth in one place everything we know about the relationship between Senator Ron Wyden and FTX. Regular readers will find plenty of new information about what Wyden did for FTX as chair of the Senate Finance Committee, and a newly unearthed $100,000 bit of campaign help the crypto industry gave Wyden in exchange. If you’re new to the Wyden/FTX story, this piece should bring you up to speed. I’ve spent a lot of time in the last year researching and writing about Wyden, FTX and Bankman-Fried. Here, I present the highlights of what I know, and links that allow the interested reader to go deeper.

U.S. Senator and Senate Finance Committee Chairman Ron Wyden (D-OR) used his considerable clout to shield now-bankrupt cryptocurrency exchange FTX from tax reporting and regulatory investigations in 2021 and 2022, a review of press reports, Finance Committee records and Securities and Exchange Commission rulemaking records show. In 2022, Wyden was rewarded by FTX, its CEO Sam Bankman-Fried (who last week was convicted on seven counts of fraud and money laundering) and associates and crypto industry allies with over $600,000 in campaign contributions benefitting Wyden.

I’ve covered at some length the FTX-related contributions to Wyden and Wyden-affiliated PACs that occurred in 2022. I’ll recap that, with news on a $100,000 crypto find, in a bit. First, though, I want to focus on what, exactly, Wyden actually did to benefit FTX and the cryptocurrency industry at large in the two years before FTX filed bankruptcy in November 2022.

To put it another way, what quid earned Wyden such a handsome FTX/Bankman-Fried quo in 2022?

The quid

Wyden chairs the Senate Finance Committee, one of the most influential institutions in our federal government when it comes to taxes, financial regulation and a whole bunch of other stuff. There are a few committees on the Hill that earn the near-universal adjective “powerful” when describing them: House Ways and Means, and Commerce and Appropriations Committees in both houses and Senate Finance. The resignation of Senator Bob Packwood (R-OR) under a hail of sexual harassment allegations in 1995 was such a big deal nationally in part because he chaired Senate Finance at the time.

Whoever chairs that committee is, by definition, among the most influential one-to-two percent of the 535 members of Congress. That is especially true for nascent industries trying to find their place in a regulatory environment that was not made for them. Industries like crypto, which heading into 2021 was a booming and little-understood way for people to buy and sell things, and store value, without the use of paper currency.*

As crypto grew in the late 2010s and heading into the 2020s, it was in a kind of regulatory no-man’s-land, especially in the United States. The most lucrative market for crypto was the U.S., but the uncertainty of the regulatory climate here made doing business directly in the U.S. problematic. That’s why Bankman-Fried, who is from the Bay Area, started FTX in Hong Kong and later moved it to the Bahamas.

And it’s also why by 2021, Bankman-Fried was focused on picking his way through, and changing, the American crypto regulatory thicket. Michael Lewis, author of the new Bankman-Fried biography Going Infinite, writes that Bankman-Fried told him, “For better or worse, my job is now thirty percent telling the regulators about what regulation should look like for crypto in the United States.”

Bankman-Fried’s focus on Washington, D.C. was accompanied by a huge influx of money from FTX and other crypto firms, but especially FTX, into shaping regulations by hiring lobbyists and lawyers and getting organized to impact federal policy like any other big American industry.

In the summer of 2021, an unexpected challenge to the industry tested crypto’s newly procured influence. Joe Biden’s infrastructure bill was barreling through Congress, and its proponents needed revenue increases to partially offset at least a little bit of the bill’s $1 trillion in new spending. Its drafters identified crypto as a potential funding source, and included language in the bill that would broaden tax reporting requirements for people and companies working in crypto. The industry said it was worried the reporting requirement would keep small operators, including miners who somehow “mine” crypto using lots of computer power and, I assume, magic, out of the business. The industry rallied its allies in Congress to stop the threat.

Ron Wyden, chair of the tax-law-writing Finance Committee, surprised many when he offered substitute language late in the legislative process that would curtail the tax reporting requirements. Wyden’s fifty-year congressional career, spanning the House and the Senate, was mostly spent as a good Democrat foot soldier. It was unusual for him to pick a high-profile fight with Biden just as the president was about to achieve a big legislative victory. But that’s just what Wyden did.

The crypto industry and its newfound allies in DC promoted Wyden’s amendment as a means to protect the “little guys” in crypto. Michelle Bond, then president of the Association for Digital Asset Markets, a new (with crypto in DC, everything was new) trade association and girlfriend of FTX co-CEO Ryan Salame, took to Twitter to urge Senators to support the Wyden language.

Wyden’s language did not, ultimately, make it into the bill. But his efforts on behalf of the crypto industry were noted at the time. On August 9, 2021, in the midst of the tax fight, Politico reported on Wyden being a crucial new ally of crypto.

“Crypto’s success with Wyden is one of the most fascinating D.C. influence developments of 2021, and one I suspect other industries will be studying throughout the rest of the decade,” Jeff Hauser, of the lobbying-tracking outfit Revolving Door Project, told Politico.

Crypto’s success with Wyden was not a one-off affair. In 2022, FTX and other industry players grew increasingly concerned with a U.S. Securities and Exchange Commission investigation into whether crypto markets complied with the country’s byzantine regulation of securities, a fancy word for something, like a share of stock, that represented partial ownership in a business. Ever since the 1929 stock market crash, the U.S. had taken great efforts to regulate securities in an attempt to protect investors. The SEC believed that some of the crypto “coins” or “tokens” represented securities and should have been subject to securities regulations.

Fear of the SEC drove much of FTX’s and Bankman-Fried’s efforts in DC. The company desperately wanted to be regulated by the less-intimidating Commodities Futures Trading Commission, which regulates markets selling “futures,” or bets on the future value of an asset. As financial market watchdog Better Markets put it, FTX “wanted the smallest, least funded and most ‘capturable’ financial regulator to get the job [of regulating FTX] so it could benefit from the form but not the substance of real regulation.”

FTX went all in on the CFTC strategy, hiring former CFTC officials, including Mark Wetjen, former CFTC Commissioner, into its government affairs and legal departments. The SEC probe, and the precedent it may set for further SEC regulation of the industry, was a direct threat to the top lobbying aim of FTX.

In March 2022, the crypto industry swung, again, into action to brush back the FEC. Eight House members sent a letter to the chair of the SEC, demanding he stop securities enforcement against the industry.

As chair of the powerful Senate Finance Committee, Wyden got his own forum. Seemingly out of nowhere, on March 7, 2022, The Financial Times ran a story that began like this:

In the story, Wyden separated himself from a bipartisan group of senators who had recently written the SEC urging it to more aggressively regulate crypto. With no apparent news hook - Wyden had not signed the senators’ letter and did not send his own - the story reads like the crypto industry responding, via its most powerful congressional ally, to the other senators’ letter, as well as what would become, or already was, an SEC investigation into the industry. Maybe I’m wrong, but the story at the very least set Wyden up, again, as an opponent of the Biden administration’s efforts to regulate crypto.

The prior year, SEC chairman Gary Gensler had said that crypto markets were “rife with frauds, scams and abuse.” Wyden stuck up for the industry in March 2022, declaring he was “on the side of the innovator,” i.e. crypto.

Wyden, one of the most powerful players in Congress, had drawn his line in the sand, warning regulators over which his committee exercised partial jurisdiction to back off crypto. The SEC failed to get a handle on crypto markets until it was too late. Less than two years later, Bankman-Fried was convicted of defrauding investors in FTX, his crypto market, of billions of dollars.

The quo

If you’ve been reading the Oregon Roundup at any point since early 2023, you’ve read plenty about me banging on about the FTX team’s lavishing of funds on Wyden and his favored causes. If you’re tired of all that, skip ahead. Otherwise, I will here lay out a timeline for the lavishing, add a bit of context, and have a newsy bit of independent expenditure by the crypto industry to help Wyden’s never-in-danger-of-losing 2022 re-election campaign, which I haven’t reported on previously.

Sam Bankman-Fried had a brief but noteworthy career as a huge political donor, giving around $70 million to candidates and causes in 2022 alone. And those are just the easily traceable contributions. Bankman-Fried biographer Michael Lewis estimates that Alameda Research, FTX’s Bankman-Fried-founded affiliate which was funneling funds, unlawfully as it turns out, at a rapid clip from FTX, loaned $1 billion to Bankman-Fried and $543 million to head engineer Nishad Singh for political and charitable causes between 2020 and 2023. Lewis divides the political giving into three categories: (1) giving intended to help make Bankman-Fried money by steering U.S. crypto regulations in a direction favorable to FTX; (2) giving intended to steer elected officials to prioritize prevention of future pandemics; and (3) giving intended to elect new members of Congress who would prioritize the future of pandemics**.

Wyden received a big, perhaps the biggest, chunk of the giving intended to influence crypto regulations, commensurate with his vast ability to impact those regulations from his perch as chair of Senate Finance.

The Bankman-Fried clan giving to Wyden began, curiously, in 2010, when Sam Bankman-Fried was only 18 and FTX did not exist, even in theory. That year, Joe Bankman, Stanford law professor and nationally recognized tax expert, gave Wyden’s re-election campaign the then federal maximum $2,500. It is unclear what Bankman’s relationship was with Wyden, if any, aside from Bankman having appeared before the Finance Committee, on which Wyden then served as a back-bencher, on tax issues. Bankman later held important, though amorphous, roles in FTX.

The Wyden donation was the largest federal political contribution Bankman had ever given, by a long shot. Bankman is the subject of an ongoing federal investigation into his role in the FTX collapse and his son’s fraud.

In April 2022, Sam’s brother Gabe Bankman-Fried, who helped direct FTX money to elected officials, gave Wyden the federal maximum donation of $2,900.

In September 2022, Wyden’s contract fundraiser - introduced as “all things Ron Wyden” to FTX agents - brokered a $500,000 contribution from Nishad Singh to the Democratic Party of Oregon’s (“DPO”) get-out-the-vote coordinated campaign. The coordinated campaign was the DPO’s effort to leverage the fundraising clout of Oregon’s democratic congressional delegation to help Democrat Tina Kotek win the closely contested governor’s race. Wyden, who wields the most clout of any federal elected official from Oregon, is the crown jewel of the coordinated campaign, and the DPO put the half-million from Singh right to use helping Kotek win a narrow victory.

I have written extensively about the Singh-DPO contribution, and I won’t belabor it here. For our purposes today, the relevant pieces of the story are that (1) The money almost certainly came not originally from Singh but from Alameda Research, the affiliate that was, unbeknownst to most anyone, draining FTX financially dry; and (2) Wyden’s spokesperson told The Oregonian, “The Wyden campaign played no role in the donation to [the DPO],” despite the existence of emails identifying the fundraiser as “all things Ron Wyden,” and the fundraiser emailing Wyden campaign staff, to their Wyden campaign email email addresses, about the contribution.

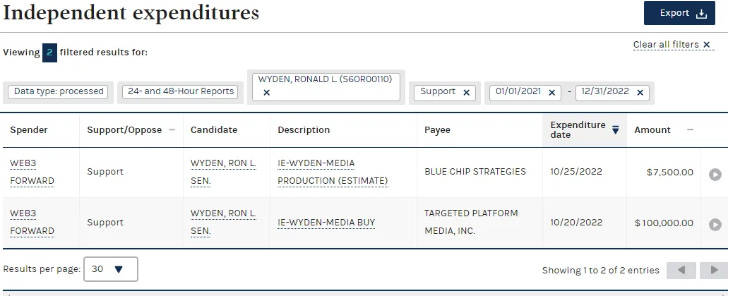

On October 26, 2022, the federal political action committee Web3Forward, reported to the Federal Elections Commission that it had spent $100,000 running ads to help Wyden win re-election, and $7,500 creating those ads. This is the campaign spending I haven’t reported on previously.

Web3Forward is a pro-crypto PAC funded in large measure by GMI PAC, which itself was co-founded by FTX co-CEO Ryan Salame, and funded by Bankman-Fried and FTX.

I think of the Web3Forward/GMI spending on behalf of Wyden as a gratuity - Wyden didn’t need the help (his re-election was never in doubt and he won by 15 points) and, if Wyden had been in a competitive race, $100,000 wouldn’t have moved the needle much, if at all, especially coming so soon before election day. It was, by all appearances, the crypto industry, led by Bankman-Fried and FTX, saying thanks for a job well-done.

The same day, October 26, 2022, about two weeks before FTX filed for bankruptcy, Sam Bankman-Fried himself contributed $2,900 to Wyden.

In 2023, as federal prosecutors waded through the FTX collapse mess, Wyden handed over to federal marshals the Sam and Gabe Bankman-Fried contributions. The DPO scrounged up enough to give federal marshals $500,000, the same amount it had received from Singh last year and promptly spent, by arranging contributions to the party from, most prominently, Ron Wyden.

So what?

It’s not necessarily illegal for people in industries benefitted by the actions or inactions of members of Congress to contribute politically to those members of Congress. (I do, however, believe that Wyden broke federal campaign finance laws by directing the $500,000 from Singh et al. to the DPO. I filed an as-yet unresolved complaint with the Federal Election Commission on that point).

The conviction of Bankman-Fried and convulsions in the crypto market, which led in part to the failing of Silicon Valley Bank and other mid-sized banks catering to crypto firms, has people wondering how all of this could happen. How could billions of paper value evaporate? How could Bankman-Fried have defrauded so many American citizens under the nose of federal regulators?

Ron Wyden’s close financial relationship with team FTX and intervention at key points on FTX’s behalf to shield it from tax and regulatory scrutiny as the company barreled toward oblivion is an essential part of the story. Wyden probably lacked the ability to singlehandedly prevent the FTX disaster, but he helped the company avoid federal scrutiny when it mattered most.

*Cryptocurrency is something I don't understand well, even after spending lots of time researching and writing about, at least from the political angle. Basically, crypto coins or tokens have value because some people agree they do, and the software that keeps track of how many coins or tokens people have is called the blockchain.

** The pandemic prevention giving is what led Bankman-Fried to spend $10 million in an unsuccessful effort to win Carrick Flynn the Democratic nomination in Oregon's newly drawn 6th Congressional District in 2022. Flynn was an EA and worked in pandemic prevention. Bankman-Fried spent just under $1,000 per vote won by Flynn.

Woops, I accidentally deleted the asterisk entries at the end. Here they are in very abbreviated form:

*Cryptocurrency is something I don't understand well, even after spending lots of time researching and writing about, at least from the political angle. Basically, crypto coins or tokens have value because some people agree they do, and the software that keeps track of how many coins or tokens people have is called the blockchain.

** The pandemic prevention giving is what led Bankman-Fried to spend $10 million in an unsuccessful effort to win Carrick Flynn the Democratic nomination in Oregon's newly drawn 6th Congressional District in 2022. Flynn was an EA and worked in pandemic prevention. Bankman-Fried spent just under $1,000 per vote won by Flynn.

Jeff: Tremendous reporting and writing. I'd like to cross-post to PortlandDissent.

Always good to know what the current market for buying a US Senator is.